Find out more about Private Equity

Reasons to invest in Private Equity : A highly attractive asset class

Investing in unlisted companies, continues to benefit from low correlation with other asset classes, making it a valuable source of diversification for investment portfolios.

Returns are generally higher than those of listed equities due to the nature of these investments, which often involve active management strategies, restructuring or growth of investee companies.

In the US, Private Equity has significantly outperformed the S&P 500 over 5, 10 and 20 years. For example, over a 20-year period, the annualised performance of private equity is +9.9%, compared with +5.9% for the S&P 500.

This higher performance is partly explained by access to private companies, often with high growth potential, and operational improvement strategies that are not always available in public markets.

Recent Private Equity investment returns outperforming listed markets

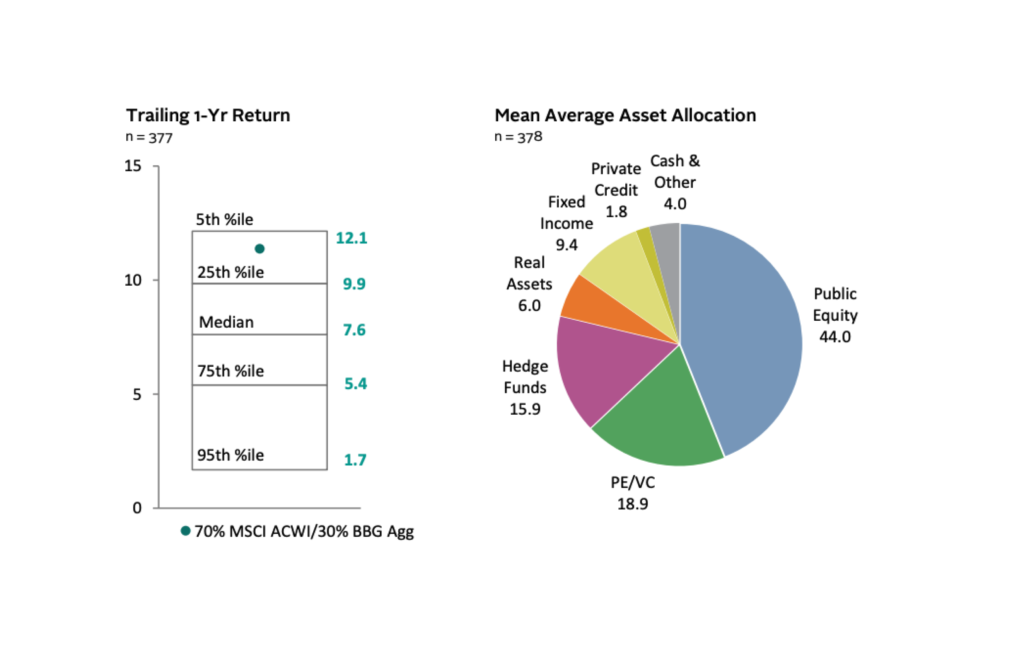

According to the latest data from Cambridge Associates for the first half of 2023, Private Equity in the US generated an annualised return of 9.8% over 20 years, outperforming the S&P 500, which returned 7.9% over the same period.

This confirms the historical trend that Private Equity investments outperform over the long term.

In Europe, according to Invest Europe, LBO funds have also delivered strong annualised returns, reaching around 15% per year over several decades, compared with 5-6% for the MSCI Europe (US PE/ VC BENCHMARK COMMENTARY / Private Investment Benchmarks / ENDOWMENTS QUARTERLY).

The opportunity to make a difference

By funding companies that you believe in and allowing them to grow, you are actively involved in turning an idea into reality. As a direct investor, you can get involved in the company’s development if you wish.

Optimal diversification of your assets

Investing in Private Equity means taking majority or minority stakes in unlisted companies.

This allows you to diversify your investments while at the same time investing in the real economy, in direct contact with the companies you support.

The aim is to make significant capital gains over the medium to long term by selling all or part of your holding when the company goes public or is sold.

And because you are one of the first shareholders, you benefit most when you succeed.

Investments in tangible assets

Private equity is not just a financial or virtual product. It gives you real meaning to your asset allocation. You invest in businesses you believe in.

The world belongs to those who invest early.

INVEST DIRECT preferences

INVEST DIRECT focuses on 3 types of Private Equity investments:

Venture capital, which finances young and often technology-based companies, is the best known. We prefer companies with a proven track record (e.g. having raised several rounds of financing).

Growth capital, which supports companies that want to increase their production capacity, expand their sales force or acquire other companies. In this case, we focus on profitable SMEs.

Leveraged transactions, where a company is sold to a group of individuals (usually the management). We could find long-term investors to provide these managers with additional equity. They would then buy the business together in a leveraged buy-out (LBO).

Risks in Private Equity investment: Loss of capital

Our vetting methods mitigate some of this risk. However, as with the stock market (e.g. Enron in the USA or WireCard in Germany), you may lose all or part of your investment.

Liquidity

These companies are privately owned and are not listed on the stock exchange. As a result, you cannot sell your shares on an organised secondary market. However, we encourage companies to organise liquidity periods. This allows you to offer your shares to other subscribers on a regular basis and in full transparency with the companies.

Valuation

Stock market listings provide a market value for your investment on a daily basis, which is not the case with Private Equity. To overcome this disadvantage, our platform provides you with an independent valuation of your holdings on a quarterly basis. However, this valuation may differ (up or down) from the price received in a liquidity event. In addition, access to our platform is restricted to qualified investors.